RGeopolitical instability in West Asia is forcing a reassessment of how India’s macroeconomic energy is measured.

As of March 2026, this instability has led to energetic macroeconomic stress. The rupee has fallen to an all-time low 95 rupees to the greenback, Indian crude oil basket touched $156.29 The Reserve Financial institution of India has injected billions of {dollars} in international alternate reserves to dampen volatility. In such circumstances, robust quarterly GDP statistics seize home exercise however typically overlook vulnerabilities associated to power imports, transport routes, and financial buffers.

In opposition to this backdrop, India is coming into the post-budget season with vital macroeconomic contradictions. Key indicators stay robust. The State Financial institution of India forecasts GDP progress of round 8.1% within the third quarter of FY26, with public capital expenditure at near 4% of GDP, holding fiscal well being on observe for a 4.3% deficit by FY27. On the identical time, exterior buffers are weakening. Overseas alternate reserves have fallen to about $709.76 billion from latest highs, with forex pressures mounting as a result of outflow of greater than $8 billion in abroad portfolios for the reason that outbreak of the battle.

Nevertheless, earnings traits are weakening. Actual wages stay depressed, family debt has risen to round 41% of GDP, and personal funding continues to lag behind state-led capital funding progress.

This divergence displays deeper modifications in India’s fiscal construction. Income buoyancy is more and more pushed by transaction-related taxation, whereas spending is tilted in the direction of capital formation. In a secure world surroundings, this mannequin can maintain progress, however when power markets grow to be unstable, its sturdiness is determined by whether or not fiscal earnings, consumption, and funding can stand up to exterior commodity shocks.

Modifications in revenue construction

India’s income construction is altering in a extra necessary path in a unstable world surroundings. Income receipts rose from 8.5% of GDP in FY16-20 to about 9.1% (PA) in FY22-25, however this improve displays restructuring fairly than enlargement of earnings taxation. The Union Finances for 2026-27 estimates whole tax income at Rs 44.04 crore, Nevertheless, a lot of the present buoyancy comes from trading-related channels. GST collections reached Rs 22.8 lakh crore in FY25, with elevated levy on monetary and cross-border transactions.

Direct taxes usually develop as extra employees transfer into secure paid employment. Consequently, income progress has grow to be depending on the amount of financial transactions fairly than income deepening.

Exterior shocks, notably rising power costs that improve transportation prices and compress family spending, can rapidly decelerate transactions. In such circumstances, fiscal fashions that depend on activity-based taxation grow to be extra delicate to geopolitical disruptions that spill over into consumption, commerce, and monetary markets.

This vulnerability has additionally been uncovered in previous shocks. The hole between projected and precise GST income widened in the course of the pandemic, forcing the federal authorities to borrow greater than Rs 2,690 crore from 2020 to 2022 to fulfill the income shortfall in states.

Impression of hovering crude oil costs

India’s fiscal system stays structurally uncovered to fluctuations in oil costs. For the reason that nation imports roughly 85-87% of its crude oil, it’s straight vulnerable to exterior power shocks as a direct transmission channel to the macro financial system.

Empirical estimates recommend {that a} $10 per barrel improve in oil costs may improve client value index inflation by about 0.2 share factors, widen the present account deficit by about $9 billion to $10 billion (about 0.4 p.c of GDP), and cut back GDP progress by practically 0.5 share factors beneath partial pass-through situations. Oil shocks even have ripple results on the fiscal system. Rising power prices will improve subsidy necessities for fertilizers and LPG, improve transportation and logistics prices, and improve spending linked to inflation.

Latest coverage responses display this transmission. Within the wake of Russia’s invasion of Ukraine, India’s crude oil basket rose from about $59 a barrel in 2019 to greater than $120 a barrel by mid-2022.

To regulate inflation, the federal government has decreased central excise responsibility on petrol and diesel by a cumulative Rs 13 and Rs 16 per liter from November 2021 to Could 2022, leading to an estimated income lack of Rs 2,200 crore. On the identical time, energy-related subsidies additionally expanded, with fertilizer subsidies growing sharply and whole power subsidies reaching practically Rs 320,000 crore.

Amid ongoing battle in West Asia, ICRA estimates that if oil costs common round $100 a barrel, India’s present account deficit may widen from round 0.7-0.8% of GDP to almost 1%, whereas authorities spending may rise by as a lot as 3.6 trillion rupees because of elevated calls for for subsidies and compensation. This highlights how power shocks are concurrently translated into exterior imbalances and financial stress.

When oil costs rise, governments usually soak up among the shock by reducing taxes and growing subsidies, compressing fiscal area. In a system that’s more and more reliant on transaction-linked taxes, such shocks may concurrently weaken consumption, cut back GST buoyancy, amplify spending pressures and trigger direct fiscal pressures.

Impression on family funds

Family stability sheets reveal necessary channels by means of which power fluctuations transmit into the home financial system.

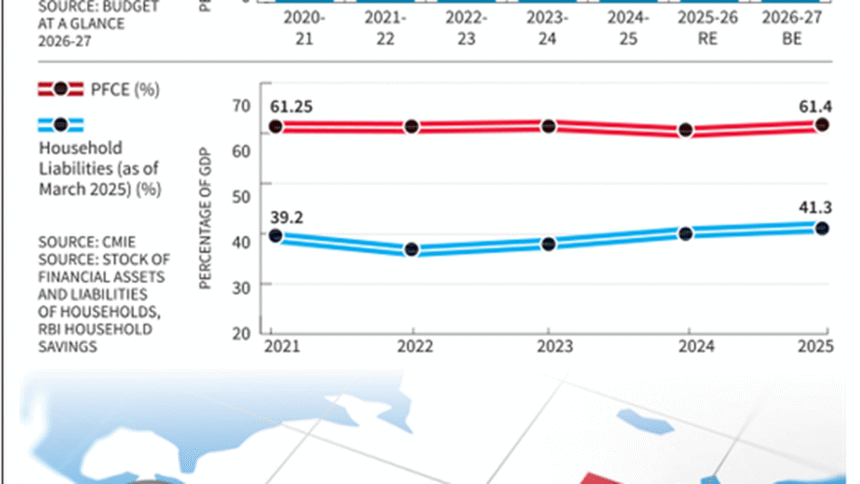

Non-public consumption accounts for about 61.4% of India’s GDP, however family debt has surged from about 36-37% of GDP in 2022 to over 41% by 2025, growing sensitivity to inflation shocks and suggesting that consumption is supported by credit score enlargement fairly than earnings progress.

Web monetary financial savings have additionally grow to be extra unstable, falling to round 3-4% of GDP in latest quarters earlier than recovering to round 7.6%, indicating weakening monetary buffers.

The influence is compounded by the shock, as disruptions to the LPG provide chain, which is greater than 60% depending on imports, have led to longer refill cycles and native provide shortages, pushing up power prices for households whilst leverage stays elevated.

On the identical time, India’s spending technique pivoted to infrastructure-led progress. Within the Union Finances for 2026-27, the efficient capital expenditure has been set at Rs 17.15 lakh crore.

Whereas such front-loaded investments strengthen long-term manufacturing capability, they cut back fiscal area for welfare stabilization. The allocation for the Mahatma Gandhi Nationwide Rural Employment Assure Act has been decreased to Rs 60,000 crore in 2023-24, 33 per cent decrease than the earlier yr’s revised estimate. By December 2022, states had already exhausted 117 per cent of obtainable funds and had excellent money owed of Rs 8,449 crore.

In a low-wage surroundings, the inflation of imported power compresses actual incomes whereas debt service obligations stay fastened. Rising family leverage due to this fact turns into a macroeconomic vulnerability, particularly when fiscal coverage prioritizes capital formation over earnings help and consumption slumps because of exterior shocks. Past family funds, geopolitical uncertainty can also be impacting company funding and credit score allocation.

Impression on the economic sector

India’s industrial turnaround is more and more concentrated in capital-intensive sectors coupled with public funding. Industrial manufacturing elevated by 7.8% in December 2025, and manufacturing elevated by 8.1% year-on-year and by 4.8% from April to December. Based on the 2025-26 Financial Survey, high-tech and medium-technology industries presently account for about 46 p.c of producing worth added.

In distinction, labor-intensive industries stay weak.

Regardless of a rise in mission bulletins, personal funding stays cautious.

Based on information from the Heart for Monitoring the Indian Financial system (CMIE), personal corporations account for practically 80% of recent mission bulletins, however solely about 9% had been accomplished in 2022-23, suggesting a restoration that expands manufacturing capability greater than wage-based earnings. Latest monetary stability assessments present that banks’ stability sheets are considerably stronger than they had been a decade in the past.

In a unstable world surroundings, this monetary energy translated into elevated danger selectivity fairly than widespread credit score enlargement.

The scarcity of business cylinders attributable to the latest LPG disaster has compelled eating places, cloud kitchens and small meals companies to shut, with gig employee unions reporting a 50 to 60 p.c drop in meals supply orders. Such shocks disproportionately have an effect on labor-intensive and casual sectors, whose incomes are straight linked to day by day calls for and lack institutional safety, despite the fact that capital-intensive sectors stay comparatively remoted inside the monetary system.

Growing exterior pressures are elevating broader questions on fiscal discretion, or the flexibility of states to soak up shocks with out abandoning their fiscal consolidation objectives. With fiscal area tied to capital spending and revenues depending on financial transactions, geopolitical turmoil can rapidly slim the area for countercyclical intervention. On this context, India must rebalance in the direction of income-driven demand, a extra resilient income base and higher power diversification, or dangers exterior shocks turning into a recurring supply of fiscal stress.

(Deepanshu Mohan is Professor and Dean of the OP Jindal World College. He’s a Visiting Professor at LSE and a Visiting Tutorial Fellow on the College of Oxford. Saksham Raj and Aditi Lazarus contributed to this column.)